Getting comfortable with the 3 priorities of household finances – budgeting, saving, investing – in that order – is no easy feat. But here’s a simple exercise that will get you started the right way.

Note: before we go further, if members are being open and honest with each other, a household should know straight away if they're in a position to think about budgeting and saving, or if they should be focusing on debt management. If the household is financially in trouble - that is - it has accumulated more debt than manageable, then it will need to first address this issue first. This post is dedicated to households that do not have debt issues. If you are suffering from unmanageable debt - I've assembled a list of helpful resources at the end of this post, below.

I’ve helped clients, friends, and family to structure household finances using the following common-sense advice. I’ve used it personally to help me budget in my lifetime – and pay off student debt, buy my first home, and build my investment portfolio; if used properly, this advice can add a wealth of insight into your own household’s spending patterns.

All you need is a basic understanding of excel, and its filters function, and your debit/credit card statements.

Step 1: download the data

“Knowledge is power”, “knowing is half the battle”, etc….

The very first and most important step for a household of any size should take is to gather the information. You can’t manage a savings and investment plan without knowing all the details.

Often, people have a good idea of what they earn, but often, only have a rough idea of what their monthly outgoings are – and knowing the full picture is the first step to planning budgeting, saving, and investment.

So the first crucial step is to get all the data together into one place. This exercise may take some time in the beginning but I promise, it will get a lot faster and easier once the household gets used to the process. Also, strangely enough, you may even start to enjoy it, like I do.

The easiest way to gather data is to download the data from your bank and credit card statements.

The goal: to create a single spreadsheet that consolidates the outgoings and incomings.

Note: while there are plenty of apps and free organisers available, I suggest doing it yourself to see all the details.

Each member of the household will want to take data from the last year starting with the most recent full expense day (so for example, I’m writing this on Tuesday July 28, so I’d take a full year counting back from Jul 27) for all debit and credit cards. This should also reflect cash withdrawals on the debit account. Most if not all credit cards like American Express and debit accounts allow custom data downloads now in .csv or excel format.

Note: if you're a heavily-cash-dependent household - that is, you spend most of your outgoings in cash, you won't be able to get as granular and insightful as to your how you spend your outgoings as the exercise below (unless you keep your receipts) - but it should be even easier for you to track the amount going out, and compare this to your income - the outgoings are simply the total of all your cash withdrawals, plus whatever you may have used on your credit/debit cards. But also, think about moving away from cash spending - as we've seen in COVID, it's a liability.

It’s important to take a year’s worth of data, because the point of the exercise is to arrive at a pretty good view of determining the household’s base outgoings, excluding the one-offs.

These one-off expenses (or incomes, like unusual bonuses, family gifts, etc.) can skew the true nature of the household’s outgoings. One-offs depend on each household, and can vary; but examples of this could include holidays (but only if you take one a year – if you frequently take holidays, you’ll want to include these costs), engagement rings, wedding presents, boiler replacements – essentially anything that is not a usual purchase. And a year will capture Christmas, holidays, birthdays, etc. – all the potential expenses you’ll need to consider when budgeting.

Step 2: categories, and sub-categories

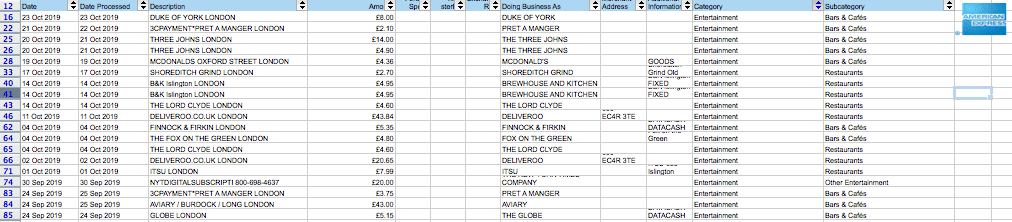

Once you have a single list of data, you can start to go through it. The data should come with its own categories – for example, American Express gives both “category” and “sub-category” columns for each entry. Here’s an example of an Amex download.

If you are interested only in the bigger picture, you don’t have to do very much here. However, I would recommend that you take the time to apply the next step, because it will make your analysis later much more meaningful.

Simply filter by each category and just check that you’re happy with the sub-categories that are popping up. For example, you’ll see McDonald’s classed as category “Entertainment” and sub-category “Bars & Cafes”. I might re-class this into sub-category “Restaurants”so that when I later filter to see how much I’m spending on “Restaurants”, I’ll know that the number includes all take-out too. (the same could be applied to Deliveroo or Just Eat items too.)

The point is to check and be happy with the sub-category classifications in a way that’s meaningful for you.

Step 3: normalise “one-offs”

The goal now is to have a scan through the lines and check for any large numbers. Separate the one-offs into its own category by relabelling these as “one-offs” or something like that.

Don’t forget to also screen for strange numbers like credit card payments – the Amex statement will also show each month’s payment as negative number line entries. You’ll want to remove these because it will skew your data.

Again, one-offs depend on the household classifying them, but you’ll want to essentially try and separate a “normal” expense versus a “one-off” or unusual expense. I don’t mean take out all the Christmas gifts and call them on-offs, because usually, you’ll buy Christmas gifts, right? But you may want to call the new sports car a one-off, or the honeymoon expense, or the Tiffany’s necklace, a one-off – that is, unless you’re frequently buying these.

This takes a small degree of personal honesty, but it’s generally pretty obvious – if you’re doing it at least on an annual basis, then it isn’t a one-off.

If say every year you take two holidays of roughly equal price, but this last year you’ve taken three, then you’ve got one extra, or “one-off” holiday. If you take a holiday every year, but last year you went all out and spent four times as much, then you’ve got the difference as a one-off. Makes sense? It’s all about what you normally do, versus the unexpected costs.

Step 4: repeat for all other credit or debit accounts

Repeat this process with your other accounts as well, checking for proper categorization and one-offs.

Step 5: consolidate (copy/ paste) into one single spreadsheet

Ideally, you’ll want to consolidate all your data into one list, which means taking your bank list and copy/pasting the data into your credit card list (or vice versa).

Often the categories may be slightly different, and/or in different columns – so make sure you clean the data first and arrange them into identical columns before you copy over.

Again, this can be done with a general understanding of excel.

This initial data cleanse and consolidation is probably the most time consuming, but usually pays off greatly with some interesting insights. In my experience, it takes about a couple hours on a Sunday to do this.

Once the data is all cleaned up and consolidated, and one-offs are re-classed, the fun can really start.

Step 6: make a simple “month P&L” (profit & loss) statement

You have a whole year’s view of how much your household is earning, versus how much it is spending, and what’s more, you have a very detailed view of how your household is spending its money. And what’s even more – you have what’s called a “normalised” view – or not including one-offs – of your spending habits.

This is powerful information – we’ll see why, and how to use it.

Usually what I would recommend now is to build, in a separate excel tab from your master costs list, a quick summary of your data showing what one month looks like. So, a simple line item list, starting at the top with your household net income, followed by each line representing a major (sub)category of costs: mortgage (rent), bills, “entertainment”, “travel”, and so on, using the (sub)categories you’ve carefully checked in the previous steps.

Note: remember to use your net incomings - so, the amount of cash from your paycheck that actually hits your bank account every month, or the amount on your weekly paycheck. (One thing that always bothered me about our world - we live day-to-day on a net expense basis - that is, our expenses are all actual prices including tax - so why do we even bother talking about our income on a gross level basis - excluding tax?)

By the way, we are showing an average here – what it looks like on average per month for your household. As for the cost lines, you can go as wide or as narrow as you’d like – that is, filter by the categories, or by the sub-categories for way more detail.

You can use a pivot table, or what I like to do is just sum up the classifications or categories (or subcategories if you’re going full out deep) and divide the sum by 12 for the monthly number and put that in my P&L. For example, if I filter for sub-category “Restaurants”, I get that total for the year by summing, and then divide by twelve.

And repeat for other categories, until my P&L covers all costs.

Note: cash withdrawals are harder to analyse given that their is no breakdown of what the cash is used on. Hopefully your cash withdrawals are mostly used for discretionary and immediate purchases, like coffees and takeaways, and can be classified mostly as such. If you're like me, I keep my cash withdrawals to an absolute minimum, so I can spot and classify cash withdrawals on my statement. Again, cash is going obsolete so I'd encourage using other payments.

So make a simple month-view P&L summary, starting with your month net income at the top, minus mortgage, minus household bills, and then minus the various (sub)categories on a month basis, until you end up with the bottom line.

Step 7: analyse

This is your monthly net income or loss, averaged, minus any one-offs.

This is the running number of your household, the steady state number, on a month by month basis.

What do you see? If you see red, then you are obviously financing your household with credit: meaning you’re facing overall debt, overdrawn credit, or overdrafts, and you’ll need to address debt management straightaway.

If you’re doing well, and you’ve got a positive net balance, then the next step is to start analysing the (sub)categories.

Step 8: budgeting

The next two things you can compare is 1) what is the proportion of your outgoings compared to your income, and 2) what proportion of your outgoings are each (sub)category?

Is your total outgoings more than 50% of your income?

Is “Restaurants” a significant portion of the outgoings?

Try to look carefully at what this monthly statement is telling you, and where you can start to make some changes. Is “Entertainment” especially high?

This is the budgeting process. Each household is different, but for every household, there will be outgoings that are non-negotiable, and plenty that are. In my experience, more often than not there will be surprises like finding out how much on average the household is spending on clothes, or makeup, or Amazon purchases, or eating out – percentage-wise, on average, per month.

Once armed with this information, the household can then start to make a solid plan and eliminate extra spending.

Step 9: don’t forget about the one-offs!

Take another look at this category, apply the same practice as above and come up with a monthly average number.

Now add it “below the line” of net monthly income. It’s important to add this below the line, as we are now adjusting the steady state number with an additional, discretionary line.

What does this look like?

Have we gone red suddenly? If so, we need to think strongly about the budgeting process. This is better news than having red at the net income stage, because typically, these are very controllable costs. If it was fate that broke the boiler, chances are, it won’t happen again in the mid-to-long term – and if it was that third holiday in Spain, then we know what we’re supposed to do here.

There is a lot of information to glean here, and you get a pretty good, average view of the financial healthiness of your household. It certainly costs time and effort upfront, but the insights in my opinion are well worth it. You’ve now got the information you need to attack certain areas of costs, in order to increase your net monthly balance.

Note: yes, there are apps that claim to be able to handle this sort of exercise for you, auto-sorting and categorising and showing you the overall expense categories, but in my experience, it's important for the household to do it themselves at the start. There will often be a lot of surprises and enlightenments about spending habits that you don't see if the app auto-sorts and categorises for you (for example, finding out that you've spend $1,000 of face cream over the year) - and also, I've yet to see an app that handles the categorisation entirely accurately, especially across different debit and credit cards. Note: at the start, many households find that the consolidation of data, especially across debit and credit card statements, can be unorganised, and confusing; sometimes a coffee purchase from starbucks will be on the debit card, and often other times, on the credit card statement. I often find - after families run this exercise - that even purchasing becomes more organised - so starbucks will only be on the credit card, etc. - and organisation is a good thing. Final note: this budgeting exercise should be done once a year, because often, the numbers change! Incomes and costs can increase, and expenses may change over time. The idea is to capture the forward, long term trajectory of the household.

Next steps: savings and investments

There are so many details regarding the next steps that I’ll have to look at each separately in another post, but essentially the next steps are really about what a household should do with its monthly surplus. There should be some detailed milestone planning that comes into effect when considering savings, and some in-depth coverage of types of investments and when to make these (primary, secondary, alternative investments).

For a household where credit is used frugally – that is, the balance is paid off each month and no negative penalties are accrued in terms of interest, late payments, and credit rating penalties, then the household should adopt the following priority:

– budgeting: as prescribed in the step-by-step process above, if this household is generating enough income, or enough outgoings control – that is, their budgeting is working- then there is surplus every month. When we have this surplus, then this household can start to think about savings.

– saving: the household should determine how much money they think they should put in a savings account for a rainy day. This is again specific to each household, but determining factors here could be – how much should we put away in case one of us is made redundant? For how long? How much should we save in case there is water damage, or the boiler breaks? The idea here is holding on to a portion of money as a safety net for all of life’s unplannable curveballs. Once there is enough in savings that the household can weather out an unforeseen event, the household can start to think about investments.

– investment: in today’s world are not the stuff of our parents’ generation. Safe “risk-free” investments like savings accounts or government bonds are no longer generating decent returns. The most important take-aways here are: any investment requires a degree of risk, so it’s great to have put away money in to savings – and the higher reward usually means higher risk. This is why investments (things like real estate, stocks, bonds, art, currencies, commodities, and so on) thought equally important as part of the overall picture, should be addressed after budgeting and saving.

Debt management

As mentioned at the very beginning of this post, we’ve assumed that debt management is not an issue for our post, but if we’re advising most households, the number one most important tenet is without doubt debt management. Often, debt errodes any chance for savings and budgeting and investing because mis-managed debt and its interest accrued will punitively penalise the account holder if payments are not made on it – not to mention plummeting credit ratings – which lead to decreased opportunities and more expensive debt (higher interest rates!)

You gotta get out of debt to be able to start saving, and investing, simple as that.

This is so important for households to conquer – paying off the balance in full each month, controlling the spending per month so that it can be paid, and making sure that they are not losing out on interest payments. Only after debt is managed properly can a household claw its way out to financial freedom and start deploying the other strategies.

This includes all debt as well – I’m talking about car payments, mortgage payments, student loans – while it’s usually impossible to pay these off in full at the start (or else why wouldn’t you just pay it off in cash, in full), the importance of paying these off quickly and timely cannot be understated.

As long as the debt repayment plan the household adopts is sensible, and reasonable (that is, no exorbitant punitive interest rates!) then the household can build the debt repayment as part of the above budgeting and planning process.

The point is – be reasonable with your debt levels, and always, always be sensible (and even cautious) when assuming more.

Not endorsing the following, but the links below could be helpful for anyone who needs debt management relief: